Estate Planning 2026: Inheritance Tax, Asset Protection

Navigating the complex landscape of Estate Planning Updates for 2026: Navigating New Inheritance Tax Laws and Asset Protection Strategies is essential for individuals and families aiming to safeguard their wealth and ensure a smooth transfer of assets to future generations.

As 2026 approaches, the world of estate planning is undergoing significant transformations, making it more critical than ever to understand the shifts in legislation and market dynamics. This guide delves into the essential Estate Planning Updates for 2026: Navigating New Inheritance Tax Laws and Asset Protection Strategies, offering clarity and actionable insights to help you secure your financial future and legacy.

Understanding the 2026 Inheritance Tax Landscape

The year 2026 is poised to bring notable changes to inheritance tax laws in the United States, impacting how estates are valued and taxed. These adjustments are not just minor tweaks; they could fundamentally alter the strategies affluent families and individuals employ to transfer wealth. Staying informed about these potential shifts is the first step toward effective planning.

One of the most anticipated changes relates to the federal estate tax exemption. While the exact figures are subject to legislative processes, projections suggest a significant alteration that could lower the exemption amount, thereby subjecting more estates to federal taxation. This shift would compel many to re-evaluate their current estate plans.

Federal Estate Tax Exemption Adjustments

The federal estate tax exemption has historically been a moving target, influenced by economic conditions and political priorities. For 2026, experts anticipate a recalibration that could reduce the amount individuals can pass on tax-free.

- Lower Exemption Thresholds: Expect a potential decrease in the federal estate tax exemption, meaning more estates might face taxation.

- Increased Taxable Estates: A lower exemption could bring a larger number of estates into the taxable bracket, necessitating proactive planning.

- Impact on High-Net-Worth Individuals: Those with substantial assets will need to review their strategies to mitigate potential tax liabilities.

The implications of these changes extend beyond just the wealthiest individuals. Even those with moderate wealth may find their estates suddenly subject to taxes they previously avoided. Therefore, a thorough review of your current net worth against projected exemption levels is paramount.

Key Changes in State-Level Estate and Inheritance Taxes

Beyond federal adjustments, state-level inheritance and estate taxes are also undergoing scrutiny and potential reforms for 2026. These state taxes vary significantly across the United States, with some states imposing substantial levies while others have none at all. Understanding your state’s specific regulations is crucial, as they can significantly impact your overall estate plan.

Some states are considering introducing new inheritance taxes or increasing existing rates to bolster state revenues. Conversely, a few states may opt to reduce or eliminate these taxes to attract high-net-worth residents. These fluctuating state laws create a complex patchwork that demands careful navigation and localized expertise.

Navigating State-Specific Regulations

Many individuals overlook state estate taxes, focusing solely on federal implications. However, state taxes can be just as impactful, sometimes even more so, depending on where you reside and the location of your assets. It’s not uncommon for an estate to be exempt from federal tax but subject to state tax.

- Residency vs. Situs: Understand whether your estate is taxed based on your residency or the physical location (situs) of your assets.

- Reciprocity Agreements: Be aware of any agreements between states that might affect how your estate is taxed if you own property in multiple jurisdictions.

- Proactive State Planning: Consider strategies like changing residency or utilizing specific state-approved trusts to minimize state tax exposure.

The dynamic nature of state tax laws means that what is advantageous today might not be tomorrow. Regular consultation with an estate planning attorney specializing in your state’s laws is essential to adapt your plan accordingly and avoid unexpected tax burdens.

Advanced Asset Protection Strategies for 2026

With the evolving tax landscape, robust asset protection strategies are more critical than ever. These strategies go beyond merely minimizing taxes; they aim to shield your wealth from creditors, lawsuits, and unforeseen financial events. In 2026, the effectiveness of various protection tools will be re-evaluated against new legal precedents and economic realities.

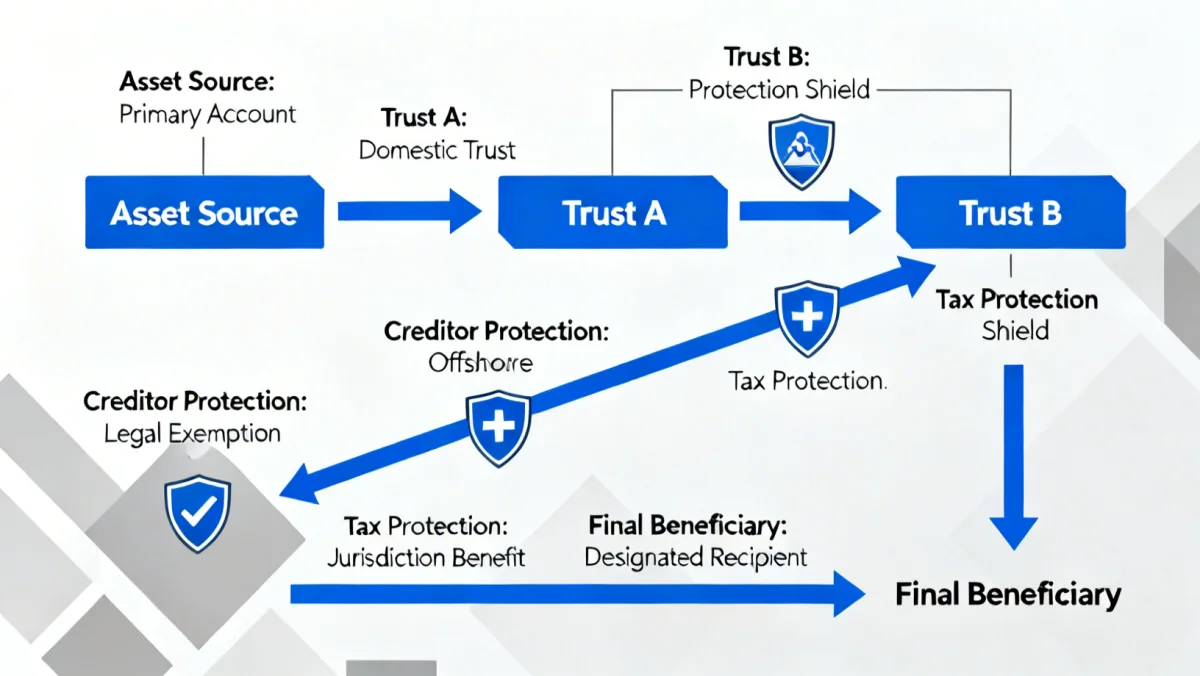

One area receiving increased attention is the use of irrevocable trusts. While these structures have long been a cornerstone of asset protection, their design and implementation will need to be meticulously reviewed to ensure they comply with updated regulations and provide the intended level of security. Furthermore, understanding the nuances of different trust types is key to selecting the most appropriate solution for your specific circumstances.

Utilizing Irrevocable Trusts Effectively

Irrevocable trusts, once established, generally cannot be altered or revoked by the grantor. This characteristic makes them powerful tools for asset protection, as the assets placed within them are no longer considered part of the grantor’s personal estate.

- Creditor Protection: Assets within an irrevocable trust are typically shielded from creditors and lawsuits, as they are legally owned by the trust.

- Estate Tax Reduction: Such trusts can remove assets from your taxable estate, potentially reducing federal and state estate taxes.

- Special Needs Planning: They are invaluable for providing for beneficiaries with special needs without jeopardizing their eligibility for government benefits.

Careful consideration must be given to the type of irrevocable trust you choose, such as a GRAT (Grantor Retained Annuity Trust) or a SLAT (Spousal Lifetime Access Trust), each with unique benefits and stipulations. Consulting with an experienced estate planning attorney is crucial to ensure the trust is structured correctly and achieves its intended protective goals.

The Role of Gifting and Charitable Contributions

Gifting strategies and charitable contributions remain powerful tools in estate planning for 2026, offering avenues to reduce taxable estates while supporting causes you care about. However, the rules governing these actions are also subject to change, requiring a fresh look at how they integrate into your overall financial plan. Understanding annual and lifetime gift tax exemptions is paramount.

With potential shifts in federal estate tax exemptions, the strategic use of gifting could become even more appealing. By transferring assets out of your estate during your lifetime, you can effectively reduce the size of your taxable estate upon death. Charitable giving, similarly, offers tax advantages while fulfilling philanthropic goals.

Maximizing Gifting Opportunities

Annual gift tax exclusions allow individuals to give a certain amount to any number of recipients each year without incurring gift tax or using up their lifetime exemption. This can be a highly effective way to gradually transfer wealth.

- Annual Exclusion Gifts: Utilize the annual gift tax exclusion to transfer wealth to heirs tax-free, reducing your taxable estate over time.

- Lifetime Exemption Use: Strategically use your lifetime gift tax exemption for larger transfers, especially if you anticipate a reduction in the exemption amount.

- Split Gifting: Married couples can combine their annual exclusions, effectively doubling the amount they can give tax-free each year.

Charitable contributions also play a significant role. Donating to qualified charities can provide immediate income tax deductions and reduce the value of your estate for estate tax purposes. Vehicles like Charitable Remainder Trusts (CRTs) or Charitable Lead Trusts (CLTs) can offer sophisticated ways to achieve both philanthropic and financial objectives.

Navigating Digital Assets and Modern Estate Planning

In an increasingly digital world, estate planning for 2026 must explicitly address digital assets. These include everything from social media accounts and cryptocurrencies to online banking portals and intellectual property stored digitally. Without proper planning, these assets can become inaccessible or lost, causing significant distress and financial complications for heirs.

The legal framework surrounding digital assets is still evolving, but some states have enacted legislation providing guidance on how fiduciaries can access and manage these accounts. Incorporating digital asset management into your estate plan is no longer optional; it’s a necessity that demands careful consideration and clear instructions.

Protecting Your Digital Legacy

Digital assets often hold significant monetary and sentimental value. Failing to plan for them can lead to disputes among beneficiaries, privacy breaches, or the permanent loss of valuable information.

- Digital Asset Inventory: Create a comprehensive list of all your digital assets, including usernames, passwords, and access instructions.

- Designated Digital Fiduciaries: Appoint a trusted individual to manage your digital assets, granting them legal authority through your will or trust.

- Utilizing Password Managers: Securely store access information using encrypted password managers, ensuring only authorized individuals can retrieve it.

It’s also crucial to consider the terms of service for various online platforms, as some may restrict access to accounts after the user’s death. Working with an attorney who understands digital asset laws can help you draft a plan that respects these terms while ensuring your wishes are carried out.

Proactive Steps for Your 2026 Estate Plan Review

Given the anticipated changes in inheritance tax laws and the need for robust asset protection strategies, a thorough review of your existing estate plan is indispensable. Delaying this process could expose your estate to unnecessary taxes, legal challenges, and unintended distributions. The time to act and adapt your plan is now, well before 2026 arrives.

This review should involve a comprehensive assessment of your current assets, liabilities, beneficiary designations, and existing legal documents. It’s an opportunity to ensure your plan aligns with your current wishes, family dynamics, and the evolving legal and financial environment. Don’t assume your old plan will suffice; proactive adjustment is key to safeguarding your legacy.

Essential Checklist for Your Estate Plan Review

Taking a structured approach to your estate plan review ensures that all critical aspects are addressed and updated in anticipation of 2026.

- Review Beneficiary Designations: Confirm that beneficiaries on all accounts (life insurance, retirement, etc.) are up-to-date and reflect your current wishes.

- Update Wills and Trusts: Ensure your will and any trusts accurately reflect new tax laws and your desired asset distribution.

- Assess Asset Titling: Verify that assets are properly titled to align with your estate planning goals and minimize probate.

- Consult with Professionals: Engage with an estate planning attorney and financial advisor to navigate complex changes and optimize your plan.

By taking these proactive steps, you can confidently navigate the complexities of Estate Planning Updates for 2026: Navigating New Inheritance Tax Laws and Asset Protection Strategies, ensuring your assets are protected and your legacy is preserved for future generations.

| Key Aspect | Brief Description |

|---|---|

| Inheritance Tax Changes | Federal and state estate tax exemptions may decrease, increasing taxable estates. |

| Asset Protection Strategies | Irrevocable trusts and other tools become vital for shielding wealth from creditors. |

| Gifting & Charitable Giving | Strategic use of annual exclusions and trusts can reduce taxable estates. |

| Digital Assets | Crucial to include digital property in estate plans for proper management and transfer. |

Frequently Asked Questions About Estate Planning in 2026

For 2026, the federal estate tax exemption is anticipated to decrease, potentially subjecting more estates to taxation. This change means that a larger portion of inherited wealth could be taxed at the federal level, urging individuals to re-evaluate their current estate planning strategies to mitigate these impacts effectively.

Asset protection strategies are crucial, especially with new tax laws. Utilizing irrevocable trusts, such as Spousal Lifetime Access Trusts (SLATs) or Grantor Retained Annuity Trusts (GRATs), can help shield assets from creditors and reduce your taxable estate. Consulting an estate planning attorney for tailored advice is highly recommended.

Yes, state inheritance and estate tax laws are also subject to potential changes in 2026. These vary significantly by state, with some possibly introducing new taxes or adjusting rates. It’s essential to understand your specific state’s regulations, as they can have a substantial impact on your estate plan.

Digital assets, including cryptocurrencies, online accounts, and intellectual property, are increasingly vital in estate planning. Without proper inclusion in your will or trust, these assets can become inaccessible or lost. Designating a digital fiduciary and creating a comprehensive inventory are critical steps for safeguarding your digital legacy.

It is advisable to review your estate plan well in advance of 2026. Proactive engagement with an estate planning attorney and financial advisor allows ample time to understand the anticipated changes, update legal documents, and implement new strategies to protect your assets and ensure your legacy aligns with current and future laws.

Conclusion

The evolving landscape of Estate Planning Updates for 2026: Navigating New Inheritance Tax Laws and Asset Protection Strategies presents both challenges and opportunities. By understanding the anticipated shifts in federal and state inheritance taxes, leveraging advanced asset protection tools like irrevocable trusts, strategically utilizing gifting and charitable contributions, and meticulously planning for digital assets, individuals can secure their financial future and ensure their legacy is preserved. Proactive engagement with experienced legal and financial professionals remains the most effective way to adapt to these changes and safeguard your wealth for generations to come.