Small Business Loan Programs 2026: Federal Funding & Grants for Growth

Securing capital through 2026 small business loan programs, federal funding, and grants is essential for entrepreneurs aiming for sustainable growth, providing critical financial pathways to expand operations and innovate.

As we look towards 2026, the landscape for small business financing continues to evolve, presenting both challenges and incredible opportunities. Understanding Small Business Loan Programs for 2026: Accessing Federal Funding and Grants for Growth is paramount for entrepreneurs seeking to expand, innovate, or simply sustain their operations in a dynamic economic climate.

Understanding the 2026 Funding Landscape for Small Businesses

The year 2026 is poised to bring new developments and continuities in the realm of small business financing. Federal funding initiatives remain a cornerstone of support, aiming to foster economic growth, job creation, and innovative ventures across the United States. Businesses must be proactive in comprehending these shifts to effectively leverage available resources.

Government agencies are continuously refining their programs to address contemporary economic needs, focusing on sectors that promise high growth, sustainability, and community impact. This includes a renewed emphasis on technology, green initiatives, and support for underserved communities. Staying informed about these priorities is crucial for aligning your business’s needs with suitable funding opportunities.

Key Shifts in Federal Funding Priorities

Federal funding priorities are rarely static. For 2026, we anticipate continued focus on several critical areas that reflect broader national economic and social goals. These shifts can significantly influence which types of businesses and projects are most likely to receive support.

- Technological Innovation: Programs supporting research and development, particularly in emerging technologies like AI, biotechnology, and advanced manufacturing, are expected to see increased allocations.

- Sustainable Practices: Businesses adopting environmentally friendly practices or developing green technologies may find enhanced access to specialized grants and loans.

- Community Development: Initiatives aimed at revitalizing local economies, supporting minority-owned businesses, and fostering entrepreneurship in rural or economically distressed areas will likely remain robust.

- Export and International Trade: Support for small businesses looking to expand into international markets, thereby boosting U.S. exports, is also a consistent priority.

Understanding these overarching themes allows business owners to tailor their applications and business plans to resonate more strongly with federal objectives. This strategic alignment can significantly improve the chances of securing funding. It’s not just about needing money; it’s about demonstrating how your business contributes to national goals.

In conclusion, the 2026 funding landscape for small businesses is characterized by a strategic alignment with national economic priorities. Entrepreneurs who meticulously research and adapt their proposals to meet these priorities will be best positioned to access the vital capital needed for growth and innovation.

Navigating SBA Loan Programs in 2026

The U.S. Small Business Administration (SBA) remains a primary resource for small businesses seeking financial assistance. In 2026, the SBA will continue to offer a suite of loan programs designed to meet various business needs, from startup capital to expansion funds. These programs often provide more favorable terms than traditional bank loans, making them highly attractive to eligible businesses.

SBA loans are not direct loans from the government; rather, they are loans issued by banks, credit unions, and other lenders, with the SBA guaranteeing a portion of the loan. This guarantee reduces the risk for lenders, making them more willing to lend to small businesses that might not qualify for conventional financing. Familiarity with the different types of SBA loans is crucial for selecting the right one.

Primary SBA Loan Offerings

The SBA provides several flagship loan programs, each tailored to specific business requirements. Understanding the nuances of each can guide businesses toward the most appropriate funding source.

- 7(a) Loan Program: This is the SBA’s most common loan program, offering financial assistance for a wide range of general business purposes, including working capital, equipment purchases, and real estate acquisition. Loan amounts can go up to $5 million.

- 504 Loan Program: Designed for major fixed assets, such as real estate or machinery, the 504 program provides long-term, fixed-rate financing. It’s ideal for businesses looking to expand or modernize their operations.

- Microloan Program: These are small loans, typically up to $50,000, provided to help small businesses and certain non-profit childcare centers start up and expand. They are often used for working capital, inventory, or equipment.

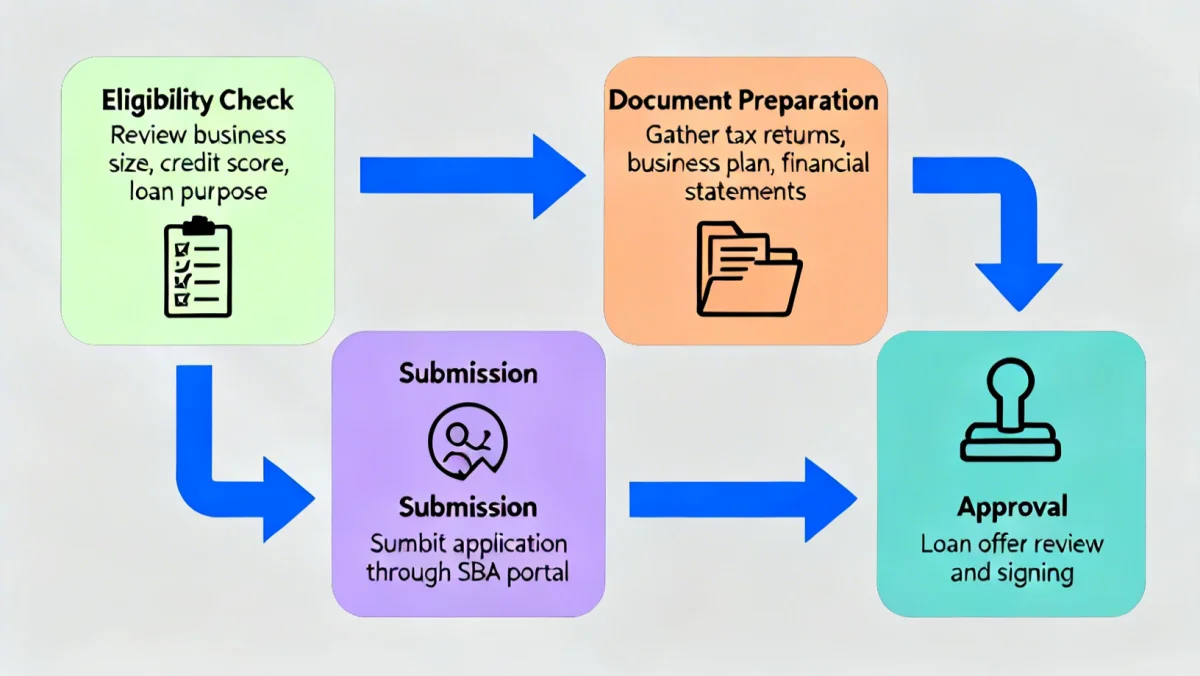

Each program has specific eligibility criteria, loan limits, and repayment terms. Prospective applicants should carefully review these details and consult with an SBA-approved lender to determine the best fit for their business. The application process, while sometimes rigorous, is designed to ensure the responsible allocation of federal guarantees.

Beyond these primary programs, the SBA also offers specialized loans for disaster relief and export activities. Keeping abreast of any new programs or modifications for 2026 will be essential for businesses looking to leverage SBA support effectively. Successfully navigating SBA loan programs requires thorough preparation and a clear understanding of your business’s financial health and projections.

Exploring Federal Grants for Small Business Growth

Unlike loans, federal grants do not need to be repaid, making them an incredibly attractive funding option for small businesses. However, grants are typically more competitive and come with stringent eligibility requirements and reporting obligations. For 2026, federal agencies will continue to offer grants focused on specific research, development, and community impact initiatives.

Grants are often awarded to businesses involved in scientific research, technological innovation, environmental protection, or social programs. They are not generally available for general business operations or startup capital in the same way loans are. Therefore, identifying the right grant opportunity requires a clear understanding of your business’s mission and its alignment with federal objectives.

Key Sources of Federal Grant Opportunities

Several federal departments and agencies are primary sources of grant funding for small businesses. These often target niche areas that contribute to broader national goals.

- Small Business Innovation Research (SBIR) and Small Business Technology Transfer (STTR) Programs: These programs, often referred to as ‘America’s Seed Fund,’ provide grants to small businesses engaged in federal research and development with the potential for commercialization. Agencies like the Department of Defense, NASA, NIH, and NSF participate.

- Department of Agriculture (USDA): Offers grants for rural development, agricultural research, and food-related businesses, especially those focused on sustainable practices or local food systems.

- Department of Energy (DOE): Provides grants for businesses working on clean energy technologies, energy efficiency, and other innovative energy solutions.

The grant application process is notoriously complex and time-consuming, requiring detailed proposals, budgets, and often, a proven track record of research or project management. Businesses should start preparing well in advance, seeking guidance from grant-writing professionals or resources provided by the granting agencies themselves. Success in securing a federal grant can provide a significant boost without the burden of repayment.

In summary, federal grants represent a powerful, non-dilutive funding source for small businesses whose work aligns with specific government research and development priorities. Diligent research and a robust, well-articulated proposal are critical for success in this competitive landscape.

Eligibility and Application Process for 2026 Federal Funding

Securing federal funding, whether through loans or grants, hinges on meeting specific eligibility criteria and meticulously navigating the application process. These requirements are designed to ensure that funds are allocated responsibly and to businesses that genuinely contribute to economic growth and federal objectives. For 2026, while exact details may evolve, the fundamental principles of eligibility and application are expected to remain consistent.

Eligibility typically includes factors such as business size (defined by revenue or number of employees), industry, ownership structure, and financial health. Grant applications, in particular, often demand a compelling narrative about the project’s potential impact and alignment with the granting agency’s mission. Understanding these foundational elements is the first step toward a successful application.

Common Eligibility Requirements

While specific criteria vary by program, several common requirements apply to most federal small business funding opportunities.

- Small Business Definition: Your business must meet the SBA’s definition of a small business, which varies by industry and is based on annual revenue or employee count.

- For-Profit Status (Loans): Most SBA loan programs are for for-profit businesses operating in the U.S. Grants can sometimes extend to non-profits with specific missions.

- Financial Health: Applicants typically need to demonstrate a reasonable credit score, sound financial management, and the ability to repay a loan (for loan programs).

- Specific Industry/Project Alignment (Grants): For grants, the business’s activities or proposed project must directly align with the granting agency’s objectives and priorities.

The application process itself demands thorough documentation and attention to detail. This often includes a comprehensive business plan, financial statements (profit and loss, balance sheets, cash flow projections), personal financial statements of owners, tax returns, and legal documents. For grants, a detailed proposal outlining the project, its objectives, methodology, and expected outcomes is critical.

It is highly recommended that businesses begin gathering these documents and preparing their narratives well in advance. Many agencies offer online portals for application submission, but the quality and completeness of the submitted materials are paramount. Seeking assistance from business advisors, lenders, or grant consultants can significantly enhance the quality of your application and improve your chances of approval. Adhering strictly to all instructions and deadlines is non-negotiable for any federal funding application.

Strategies for Maximizing Your Chances of Approval

Securing federal funding is a competitive endeavor, necessitating a strategic approach to stand out from other applicants. Simply meeting the basic eligibility requirements is often not enough; businesses must actively demonstrate their viability, potential for growth, and alignment with federal objectives. For 2026, emphasizing a strong business case, meticulous preparation, and effective communication will be key to maximizing approval chances.

A well-articulated business plan that clearly outlines your market analysis, operational strategy, management team, and financial projections is fundamental. Lenders and grant reviewers look for businesses with a clear vision, a solid understanding of their industry, and a realistic path to success. Generic applications seldom succeed; personalization and specificity are vital.

Key Strategies for a Successful Application

To enhance your application’s appeal, consider these strategic moves:

- Develop a Robust Business Plan: This document should be compelling, showcasing your business’s unique value proposition, market opportunity, and how federal funds will be utilized to achieve specific, measurable goals.

- Strengthen Financials: Ensure your credit score is strong, and your financial statements are accurate and up-to-date. Demonstrate a clear ability to manage finances responsibly and, for loans, to service debt.

- Seek Expert Guidance: Consult with SBA resource partners (like SCORE or Small Business Development Centers), experienced lenders, or professional grant writers. Their expertise can be invaluable in refining your application.

- Align with Federal Priorities: Tailor your application to highlight how your business or project contributes to current federal objectives, such as job creation, technological advancement, or community development.

Beyond the initial application, building relationships with lenders and understanding their specific preferences can also be beneficial for loan programs. For grants, attending webinars or workshops hosted by granting agencies can provide insights into their expectations and common pitfalls. Follow-up, where appropriate, and be prepared to answer questions and provide additional documentation promptly. Presenting a clear, concise, and professional application package is a direct reflection of your business’s professionalism and attention to detail, significantly influencing the perception of reviewers.

Beyond Federal: State and Local Funding Opportunities

While federal programs are significant, small businesses should not overlook the wealth of funding opportunities available at the state and local levels. Many states, counties, and cities offer their own loan programs, grants, and incentives designed to support local economies, specific industries, or underserved populations. These programs often have less stringent requirements than federal initiatives and can be more accessible for smaller, community-focused businesses.

These localized funding sources are particularly valuable for businesses that may not fit the criteria for broader federal programs or those seeking smaller amounts of capital. They often aim to stimulate local job growth, encourage specific types of development (e.g., downtown revitalization, green initiatives), or support local startups. Researching these opportunities requires a localized approach, often starting with state economic development agencies or municipal business support offices.

Identifying Localized Funding Sources

Discovering state and local funding involves targeted research and connecting with community resources.

- State Economic Development Agencies: Most states have agencies dedicated to promoting economic growth, which often manage various loan and grant programs.

- Local Chambers of Commerce: These organizations are excellent resources for information on local business incentives, grants, and networking opportunities.

- City and County Business Development Programs: Many municipalities offer programs to attract and retain businesses, sometimes including specific funds for businesses located in designated zones or those creating jobs for local residents.

- Community Development Financial Institutions (CDFIs): These are specialized financial institutions that provide financial services to low-income communities and individuals who lack access to financing from mainstream institutions. They often offer small business loans with flexible terms.

The application processes for state and local programs can vary widely, but generally, they will require a business plan, financial statements, and a clear description of how the funds will be used and their anticipated local impact. Networking within your local business community and engaging with local government representatives can also open doors to unadvertised opportunities or provide valuable insights into application strategies. Combining federal, state, and local funding can create a robust financial foundation for sustained growth.

The Future of Small Business Funding: Trends for 2026 and Beyond

Looking ahead to 2026 and beyond, the landscape of small business funding is expected to continue its dynamic evolution, driven by technological advancements, changing economic priorities, and shifting entrepreneurial needs. Understanding these emerging trends is vital for businesses to position themselves effectively for future capital access. Traditional funding avenues will coexist with innovative financing models, offering a broader spectrum of options.

One significant trend is the increasing role of FinTech (financial technology) in streamlining the loan application process and expanding access to capital. Online lenders and alternative financing platforms are becoming more sophisticated, offering quicker decisions and more tailored products, often leveraging AI and big data for underwriting. This can be particularly beneficial for businesses that may not fit traditional banking criteria.

Emerging Trends in Small Business Financing

Several key trends are shaping the future of small business funding:

- Increased Digitalization: The shift towards fully digital application processes, from initial inquiry to fund disbursement, will continue, making financing more accessible and efficient.

- Focus on Impact Investing: Investors and funding programs are increasingly prioritizing businesses that demonstrate positive social and environmental impact alongside financial returns.

- Alternative Financing Models: Beyond traditional loans and grants, options like revenue-based financing, crowdfunding, and venture debt are gaining traction, offering flexible alternatives tailored to specific business models.

- Personalized Funding Solutions: Data analytics will enable lenders to offer more personalized financing products, better matched to a business’s unique risk profile and growth trajectory.

Furthermore, government programs are likely to adapt to these trends, potentially incorporating more agile funding mechanisms and collaborating with private sector FinTech companies. Businesses should remain agile, continuously researching new funding models and platforms that emerge. Developing a strong online presence and maintaining transparent financial records will become even more crucial for engaging with these digital-first financing solutions. The future promises a more diversified and accessible funding ecosystem for small businesses, provided they stay informed and adaptable.

| Key Funding Area | Brief Description |

|---|---|

| SBA Loan Programs | Government-guaranteed loans (7a, 504, Microloans) offering favorable terms for various business needs. |

| Federal Grants | Non-repayable funds for specific research, innovation, or community impact projects (e.g., SBIR/STTR). |

| Eligibility & Application | Crucial steps include meeting size standards, demonstrating financial health, and submitting detailed proposals. |

| State & Local Funding | Additional loans, grants, and incentives from state and municipal agencies, often with localized focus. |

Frequently Asked Questions About Small Business Funding

Primary federal funding includes Small Business Administration (SBA) loan programs, such as 7(a), 504, and Microloans, which are government-guaranteed. Additionally, various federal agencies offer grants, like the SBIR/STTR programs, for specific research and development initiatives, which do not require repayment.

Federal grants are typically highly specialized, often targeting businesses in specific industries like technology, scientific research, healthcare, or environmental solutions. They require your project to align with the granting agency’s mission. General operational costs for most businesses are usually not covered by federal grants.

SBA loans are characterized by a government guarantee, reducing risk for lenders and often resulting in more favorable terms, lower down payments, and longer repayment periods compared to conventional bank loans. They also cater to businesses that might not qualify for traditional financing due to stricter bank criteria.

Key documentation includes a comprehensive business plan, detailed financial statements (P&L, balance sheet, cash flow), personal financial statements for owners, federal tax returns, and legal business documents. For grants, a robust project proposal outlining objectives and methodology is essential.

Absolutely. Businesses should investigate state and local government programs, which often provide tailored loans and grants for local economic development. Additionally, alternative financing options like crowdfunding, venture capital, angel investors, and community development financial institutions (CDFIs) are increasingly viable choices.

Conclusion

Navigating the complex world of small business financing in 2026 requires diligence, strategic planning, and a clear understanding of the diverse funding avenues available. From robust federal loan programs and competitive grants to localized incentives and emerging alternative financing models, entrepreneurs have a wealth of options to explore. By meticulously preparing applications, aligning with governmental priorities, and seeking expert guidance, small businesses can significantly enhance their chances of securing the capital necessary for sustained growth and innovation. The future holds promising opportunities for those prepared to seize them.